Rapid Reports

Equity Challenges and Opportunities in the Revised FAFSA

The FAFSA is available to all students regardless of demographic and socioeconomic background, but it is particularly helpful for student groups historically disenfranchised from postsecondary education. FAFSA provides access to subsidized student loans, work-study, Pell grants, and other college scholarships and grants to meet students' financial needs. The average cost of attending college, including tuition, required fees, books, and supplies, is $36,436 per year. As the median family income is $74,580, college costs are almost universally burdensome, especially for disadvantaged groups. The revised FAFSA form aims to increase accessibility and equity but has faced rollout challenges, creating financial uncertainty for institutions and vulnerable students.

THE PROBLEM

The New FAFSA form was expected to be unveiled by October 2023. However, it was delayed until December 2023 because of technical glitches and incorrect calculations. As a result, students would appear to have more money [assets] than actually true. The Student Aid Index (SAI) calculation guidelines are expected to consider inflation for each year moving forward. The revised means test is expected to capture low-income students and families further. With the formula fixed on January 28, 2024, the first batch of information was anticipated to be ready in March 2024. Instead, the Department of Education reported concerns about inconsistent data provided to them by the IRS impacting 5% of previously submitted applications and an unknown percentage of new applications.

HIGH HOPE FOR FAFSA

The new form was expected to increase IRS compatibility with the Department of Education, seamlessly sharing financial data between the institutions. The new form promoted a shorter and more straightforward process (from 108 to 36 questions), thus making it easier for students and their families to navigate the annual pre-college ritual intending to increase the likelihood of a student enrolling in college and persisting to graduation.

The new form was expected to increase IRS compatibility with the Department of Education, seamlessly sharing financial data between the institutions. The new form promoted a shorter and more straightforward process (from 108 to 36 questions), thus making it easier for students and their families to navigate the annual pre-college ritual intending to increase the likelihood of a student enrolling in college and persisting to graduation.

The FAFSA revisions are expected to broaden eligibility criteria, capturing students previously excluded from financial aid programs (students experiencing homelessness, formerly in foster care, formerly incarcerated, formerly enrolled in a for-profit college, and students with drug convictions). This fundamentally equitable and wider net will significantly improve access to financial aid for a wide range of students once caught in the crosshairs of societal ills.

The revised forms also anticipate an increase in eligible Pell Grant recipients, expanding its reach to approximately 610,000 new students from low-income backgrounds. Changes will lead to more families automatically qualifying for the maximum Pell Grant ($7,395). These “income protection allowances” prescribe a generous formula intended to adjust for inflation, protect families' income, and shield more of a student's income from the traditional formula, raising the protected income (20%) of parents, the income of (35%) dependent students, and the income (60%) of students with children. These increases in aid eligibility cannot be understated, considering the skyrocketing rate increase of college tuition since the 1970s. The changes will help address educational disparities felt by several groups, including first-generation, racialized minority students, veterans, and women-identifying students, ultimately increasing diversity on our college campuses.

UNDERMINING EQUITY

The rollout exacerbated higher education access issues. Financial aid accessed through FAFSA plays a crucial role in reducing disparities in higher education attainment. Successful attainment of a degree provides higher earnings and lower unemployment rates throughout a lifetime, with college graduates earning $1.2 million more on average. Early FAFSA filing has been found to lead to higher financial aid awards and an increased likelihood of college completion. However, filing late is associated with a lower likelihood of success in postsecondary school. These delays raise questions about affordability for vulnerable low socioeconomic status, first-generation, women-identifying/gender nonconforming, and immigrant students.

In 2020, as few as 59.7 percent of Asian students and as many as 84 percent of Black students completed the FAFSA, signaling disparities in FAFSA completion rates among different racial and ethnic groups. Given the historically high utility of the FAFSA among minorities and women (74.2%), they are also likely to be heavily impacted by a poorly executed rollout and implementation of the new form, exacerbating existing disparities in access to financial aid and higher education.

IMPACTS AND IMPLICATIONS

A delayed rollout, coupled with many states' “first come, first served” distribution approach, poses another barrier to families whose forms may be late. First-year community college students are less likely to file a FAFSA and are two times more likely than their 4-year public and private counterparts to file their FAFSA late. On average, students who filed later received 60 to 70 percent less state and/or institutional aid than students who filed on time. A system that prioritizes those with quicker access and resources perpetuates the inequality it is designed to minimize, potentially leaving many vulnerable populations under-resourced.

Until recently, mixed-status families, which include children with social security numbers and parents without, were slow to benefit from the form’s revisions. Students with social security numbers could more easily enroll, while parents with ITIN faced barriers. The increase in enrollment in recent years has been due largely (80%) to students from immigrant families.

The decline in FAFSA completions could have significant implications for higher education institutions and student enrollment rates. This is especially true for specialized institutions such as HBCUs, private, tribal, and women’s colleges. These institutions are generally smaller, have limited access to capital, and attract a more targeted student population, making them more susceptible to adverse impacts in a changing financial landscape.

AN IMPERATIVE TO GET FAFSA RIGHT

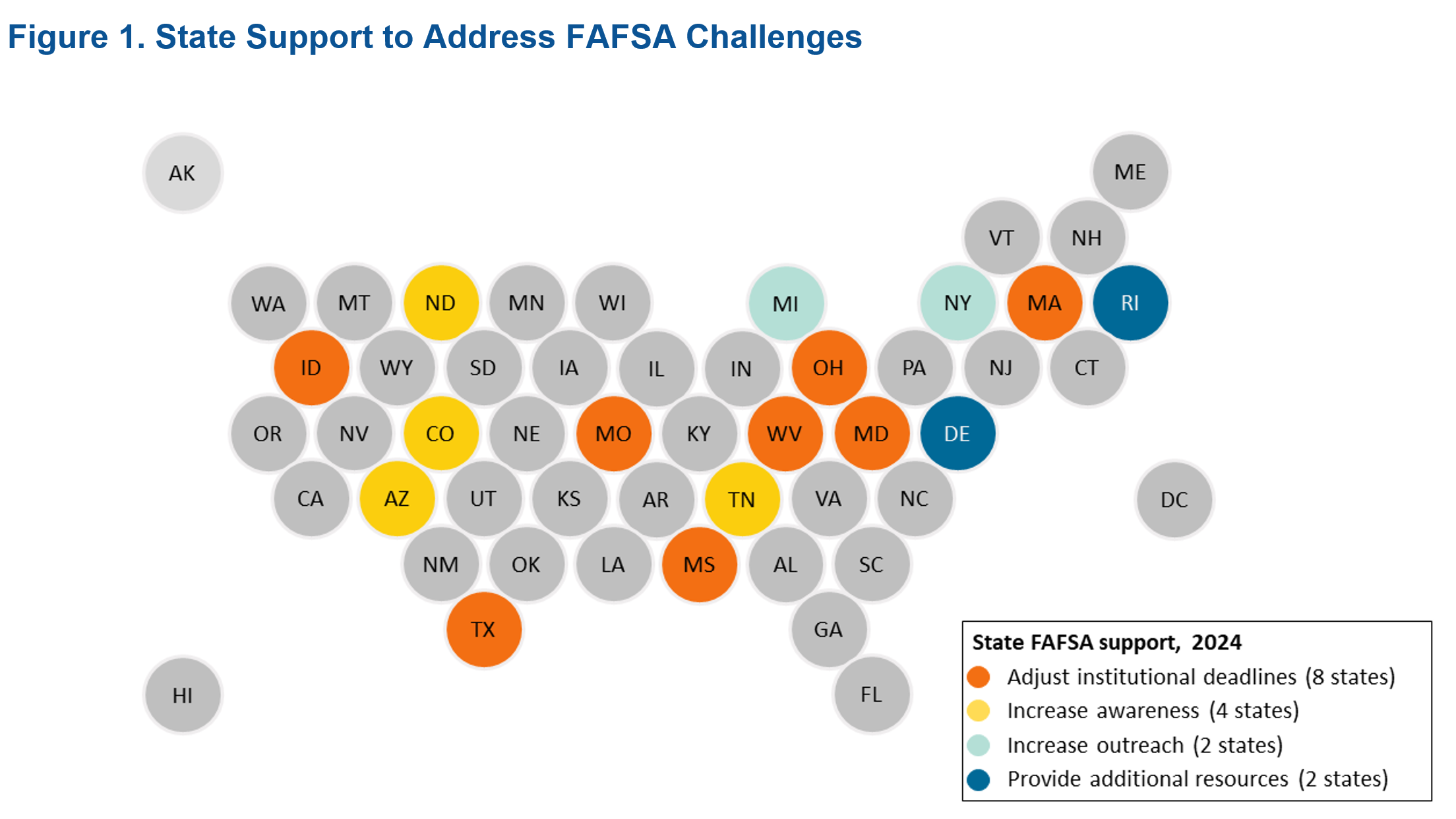

As colleges and universities determine how to provide access and opportunities to students who may be affected until the federal government resolves the form issues, states are stepping in to provide additional resources (DE, RI), increase outreach (MI, NW), raise awareness (AZ, TN, CO, ND), and adjust institutional deadlines (ID, MD, MS, MO, OH, TX, WV) to mitigate the impacts of the delay (Figure 1). As a result, more than 135 colleges and universities nationwide have extended their commitment deadlines. Federal government measures to remedy the situation include the Better FAFSA Better Future Roadmap tool by the Federal Student Aid (FSA), designed as a resource and training guide for families, schools and institutions, and other stakeholders. A soft launch approach was instituted to address emerging concerns as they arose rather than all at once. Additionally, federal financial aid experts and internal concierge services were dispatched to HBCUs, tribal colleges, and other historically low-resourced institutions for support and training as part of the rollout.

Federal government measures to remedy the situation include the Better FAFSA Better Future Roadmap tool by the Federal Student Aid (FSA), designed as a resource and training guide for families, schools and institutions, and other stakeholders. A soft launch approach was instituted to address emerging concerns as they arose rather than all at once. Additionally, federal financial aid experts and internal concierge services were dispatched to HBCUs, tribal colleges, and other historically low-resourced institutions for support and training as part of the rollout.

When fully accessible, the revised FAFSA will make 1.5 million more people eligible for the maximum Pell Grant, broadening access to higher education. If the FAFSA can fulfill its expectations, it can potentially change the lives of more than 17 million students in the long term.

POLICY RECOMMENDATIONS

The FAFSA rollout has left students questioning whether or not to continue their post-secondary education, enroll in a community college rather than a four-year college or university, or begin their post-secondary studies at all. Although community colleges may see steady or even increased student enrollment as a result of this problem, four-year universities and colleges serving many Pell-eligible students may be left scrambling to redeem their enrollment numbers for the 2025 academic year. This issue has created significant financial uncertainty for higher educational institutions and may be significantly altering the life trajectories of our most vulnerable student groups. To re-right these inequitable burdens, we recommend the following: